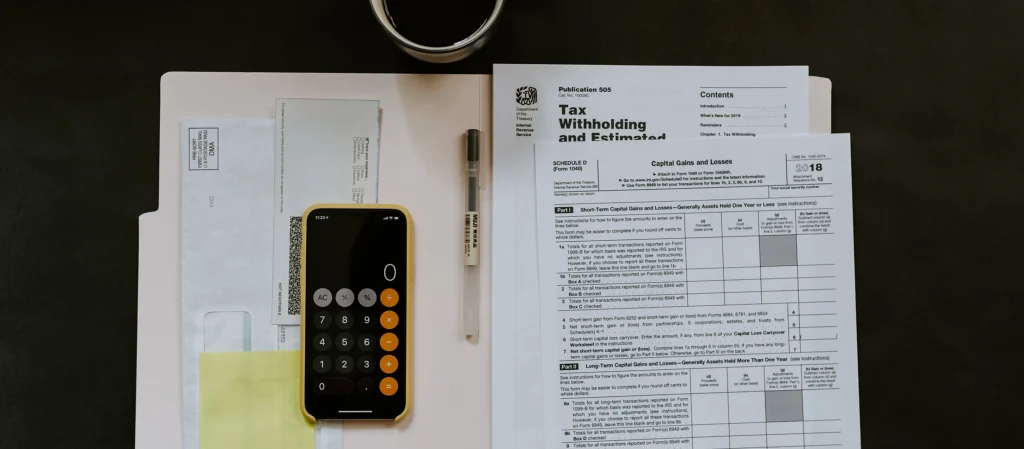

Around this time last year, we went over taxes. And in case you haven’t filed your taxes yet, we’ll go over them again today.

5 Things to Consider As you file (or get ready to), there are a few things to keep in mind. 1. The third stimulus check.

If you’re one of many who got the third stimulus check last year, remember, the money isn’t considered taxable income. So, other than checking the box on the form confirming that you already received the direct deposit or check in the mail from the IRS, there’s no need to report it as income when you file.

Now, if you’re someone who didn’t receive it, and you believe you should have, there’s something you can do when you file this year. It’s called the Recovery Rebate Credit. And you can claim it to get the check you never received.

Keep in mind, this won’t work for you if you weren’t eligible to receive the stimulus… Like, if your income was too high or you can be claimed as a dependent. So, before you claim the Recovery Rebate Credit, make sure you’re eligible.

2. Itemizing may work out better for you. Last year, the standard deduction—which is the amount the IRS automatically deducts from your taxable income—was $12,550 for individuals or married couples choosing to file separately, $18,800 for those who file as head of household, and $25,100 for married couples filing jointly.

Now, many of us don’t even think twice about whether we should go standard or itemize. But several things are tax deductible. So, it’s at least worth doing the math… If you spent more than 7.5% of your adjusted gross income (AGI) in 2021, any expenses you have above that are tax deductible.

Your AGI is your gross income after subtracting pre-tax deductions you made during the year, such as health insurance through your employer or any contributions to your 401(k). This would not include a Roth 401(k), 403(b), or 457(b), if you’re wondering.

So, if your AGI is $30,000 a year, 7.5% of $30,000 would be $2,250. If you spent $2,750 on qualified medical expenses, such as prescription glasses/contact lenses, medications, dental cleanings, or insurance premiums you paid using after-tax dollars, then $500 would be tax deductible ($2,750 – $2,250 = $500).

If you donated or gave to a 501(c)(3), that’s also tax deductible. Those would be any organizations like charities or churches.

If you contribute to a health savings account (HSA), that’s tax deductible, too.

And if you are a homeowner, you can deduct your property taxes up to $10,000 ($5,000 if married and filing separately), private mortgage insurance (unless your AGI is more than $109,000 or or $54,500 if married and filing separately), and mortgage interest payments.

So, if these home-related payments cost $17,000, and you donated $4,700 and contributed $3,500 to the HSA plan you have, that’s $25,200—a little more than the $25,100 standard deduction for a married couple, and much more than the standard deduction for heads of household, individuals or married couples filing separately.

Just always remember to keep good records. Keep your receipts and make copies, in case you’re ever audited.

That includes donations. The charity or organization you gave to should provide you with a tax receipt. And you should always have clear pictures of everything you donated.

There are plenty of ways you can do this, but CamScanner is an app you can use to easily turn a bunch of photos into one PDF. I use it for just about everything. (If you have an Android, you can check it out here. If you have iOS, you can check it out here.

3. Doing taxes on your own isn’t as hard as you think.

Filing your taxes may not be quick and painless, but it may not be as difficult to do as you may think.

You don’t have to be an accountant by trade to file taxes on your own. In fact, there are plenty of tax filing software programs that guide you every step of the way. There’s TaxAct, TurboTax, H&R Block, the list goes on. And the IRS has a list of software you can use to file for free.

Click here, if you want to find out more. If your tax situation isn’t too complicated, I strongly encourage you to learn about filing on your own. You may save yourself some money.

At the end of the day, though. Do what you are most comfortable with. If you will have peace of mind by having a professional do your taxes, then go with that option.

4. Don’t put your taxes off until the last minute.

There’s still a few weeks left to file taxes. The deadline is now April 18. But that doesn’t mean you should wait.

Again, taxes don’t take forever to file, but they do take a little bit of time and diligence. Give yourself some breathing room. That way, you’re not rushing.

If you’re anything like me, you’ll make a mistake (or two) if you rush, or you’ll forget something. So, start sooner rather than later, even if you don’t think you’ll need that much time to do your taxes.

5. Double-check everything before you click the button, and save your documents.

It may sound like a no-brainer, but before you click “File,” or “Finish,” go back and review your work.

Mistakes happen. Even if you took your time and were very careful every step of the way, you could’ve easily missed something.

Nobody’s perfect… Not even the professionals. So, even if you don’t think you made any errors, just take the few minutes it requires to go back and check. It could save you a lot of time, trouble, and money down the line.

Double-check your taxes the next day. This way, your brain and eyes are fresh.

And be sure to save everything. Save your W-2(s), 1099(s), 1098(s)… any and everything. And, yes, your 1040 return, of course. Even if you know you made no mistakes, you may be audited in the future. So, be sure to save these documents, including your receipts if you itemize, for at least the next three years.

Happy filing!

With gratitude,

Melody C. Kerr, MS

Writer, Editor & Financial Coach